This is the fifth article in a series of blog posts in which we introduce the concepts of knowledge-based lending for SME business. In this article, we introduce the monitoring process and the early Warning System. Those process steps are essential for the successful execution of SME lending. While each financial institution needs to conduct a thorough risk assessment and approval, the actual monitoring of the exposure it is equally if not more important. Clients will experience challenging situations over the life of a transaction and are in need for support from their financial institution.

We have integrated a detailed monitoring process into the development of Q-Lana, the digitization platform for knowledge-based lending. This allows the early discovery of problems developing with lending exposures, far before an actual payment default. We have developed Q-Lana as a comprehensive, fully customizable and intuitive, filled with smart tools and analytics to support financial institutions. For more information about Q-Lana, please read below and contact us

Q-Lana enables financial institutions to develop sound credit-monitoring and risk-mitigation capabilities. The earlier a financial institution identifies and responds to deterioration of credit risk, the better is the possibility to avoid problems, including defaults. Q-Lana identifies risky customers and exposures far before they experience payment problems and can easily differentiate between inability and unwillingness to service a loan. Critical customers can be placed on an internal watch list, to allow a more thorough monitoring of the relationship and the early development of mitigating solutions. This also helps financial institutions to support its clients during critical phases where they are in urgent need for such support.

Monitoring Process

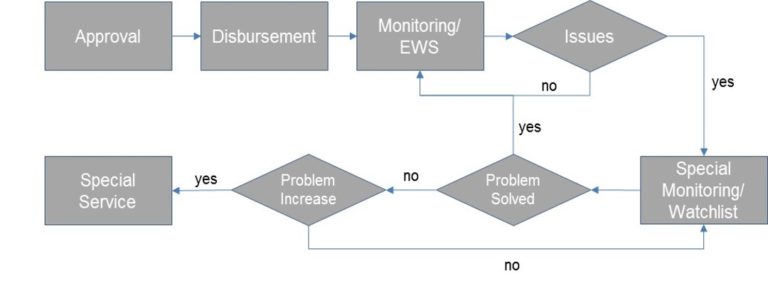

A financial institution shall focus on the monitoring of the borrowers right after the disbursement. This relates to the process of regular monitoring of performing loans. The key steps of the regular monitoring are summarized in the following picture

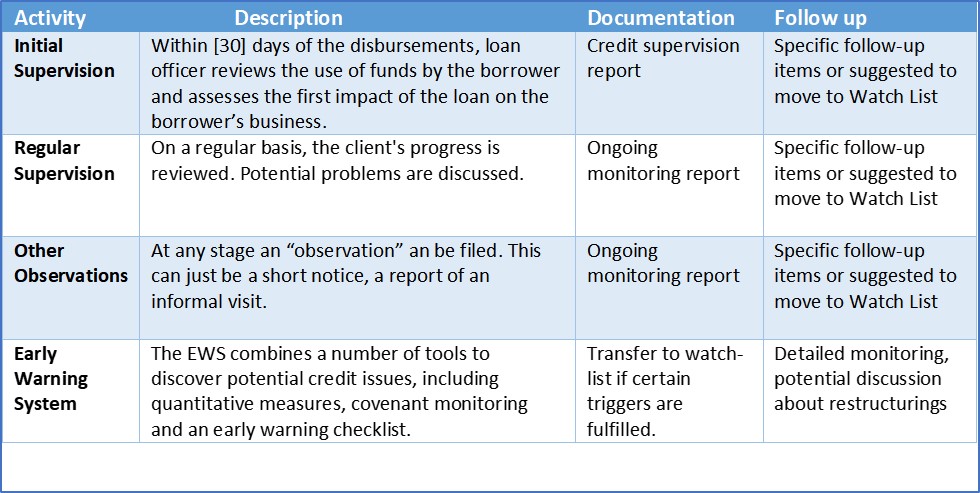

There is high importance for the monitoring, especially of long-term exposures. It is quite common that clients will experience financial or operational difficulties over the course of a longer credit exposure. Q-Lana has developed a structured process for the monitoring of exposures after disbursement. The specific process can be adjusted for the requirements of a financial institution. An example of the necessary steps is provided in the following table:

Initial Supervision Report: A financial institution requires the loan officer to conduct a follow-up visit within a certain number of days after the disbursement of the loan. This is primarily serves the purpose to verify the actual use of funds and to assess the project performance with the newly injected funds. The loan officer is required to comment on any observation be it positive or negative and to verify whether the conditions that were used to justify the approval are still valid. The form provided through Q-Lana has space for suggested follow-up items. Q-Lana will define internal tasks for each of those follow-up items to ensure that they are timely addressed. The exposure can be moved to watch-list.

Monitoring – Ongoing Monitoring: subsequent to the initial visit a regular monitoring process is started the by the loan officer. The rules of the specific institution define the frequency of such monitoring visits. For borrowers of weaker credit quality, such meetings shall happen on a more frequent basis. In each of these visits, the client’s performance is assessed and compared to the information given here in the initial loan application. Any comments or observations are noted in a report. Specific follow-up items can be set and tracked. In addition, the loan officer needs to suggest the time for the next follow-up visits and comments on the need to move the borrower to the internal watch-list.

Monitoring – Other Observation: in addition to the regular reporting’s, there is the possibility to submit “Other Observations”. This can include informal visits, observations or comments made “on the street”, reference to products, news or any other relevant information.

Early Warning System: With an effective Early-Warning System (EWS), credit losses as well as capital requirements can be reduced through de-risking. This will improve the institution’s capacity to take risk, increase returns and improve the capital productivity. For the client, the benefits include lower pricing as well as the active support from a qualified expert in the management of critical situations. The EWS is well integrated into the monitoring process of Q-Lana

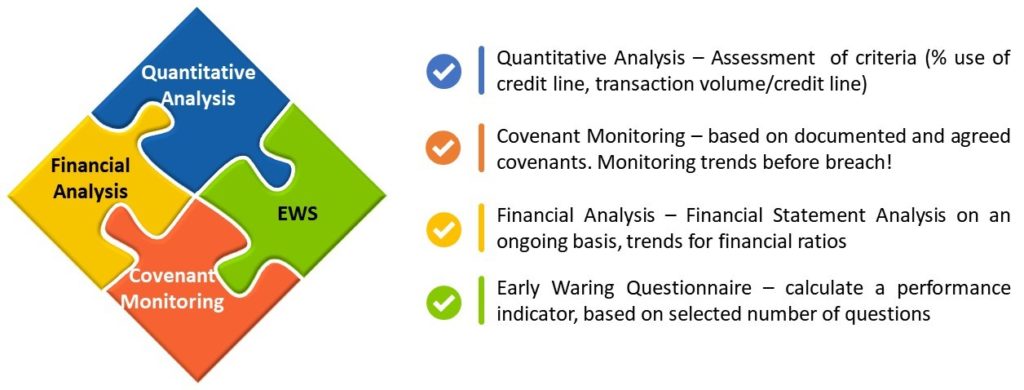

Q-Lana has integrated the EWS into the standard procedures and allows the institution to identify borrowers at risk through a structured monitoring process and the integration of warning signals. The Q-Lana EWS is built on several categories of indicators, allowing the identification of critical exposures based on electronic information/automated triggers, expert knowledge about the exposure, as well as external information. The categories are:

- Quantitative Criteria – the EWS analyzes the utilization of credit lines by borrowers, borrowing activities, cumulated arrears days and other indicators. Early warning indicators are triggered if certain patterns are discovered. For example, as soon as the utilization reaches certain limits and remains at that level, the exposure is flagged as riskier.

- Covenant Monitoring – the loan documentation might include affirmative and negative covenants, representations and warranties and other requirements. The monitoring of the compliance with these covenants is part of the EWS. Here, not only the breach of certain covenants is monitored but also the absolute value of quantifiable covenants. In this way, trends can be assessed allowing to identify weakening credit quality at early stages.

- Financial Analysis – on a regular basis, the institution receives financial information from clients. This financial information is tracked within Q-Lana and assessed through the review of certain ratios. At the same time, the institution can update the internal rating system with the new financial data, allowing the calculation of new rating values and incorporating the trends of the rating development into the EWS

- Early Warning Questions – Q-Lana has developed an early warning questionnaire which is part of the monitoring package. Loan officers can apply this questionnaire during the regular monitoring visits or when a visit is requested through the placement on watch-list. Details about the assessment questionnaire can be found in the attachment.

- Early Warning Monitor – all observations of the EWS are summarized in a dash dashboard which visualizes the specific monitoring results categorized along the line of the above-mentioned criteria

Internal Watch List – Special Monitoring: if an exposure is identified through the monitoring process as deteriorating or critical, it is placed on the internal watch-list. The number of days this exposure is placed on watch-list is tracked. It is required to prepare a special assessment of the exposure considering the reasons for placing it on watch list. Based on this initial assessment, the next steps are defined, which can include (in order of severity):

- Removal of the client from the list as the identified issues have been deemed mitigated

- Keeping the client on watch list for a more frequent monitoring procedure

- Developing measures for risk mitigation in order to improve the risk profile of the exposure and/or support the client in the recovery from a current problem

- Moving the clients to special servicing/recovery, in case the client is in default and issues have been too severe for a return to normal conditions in the future

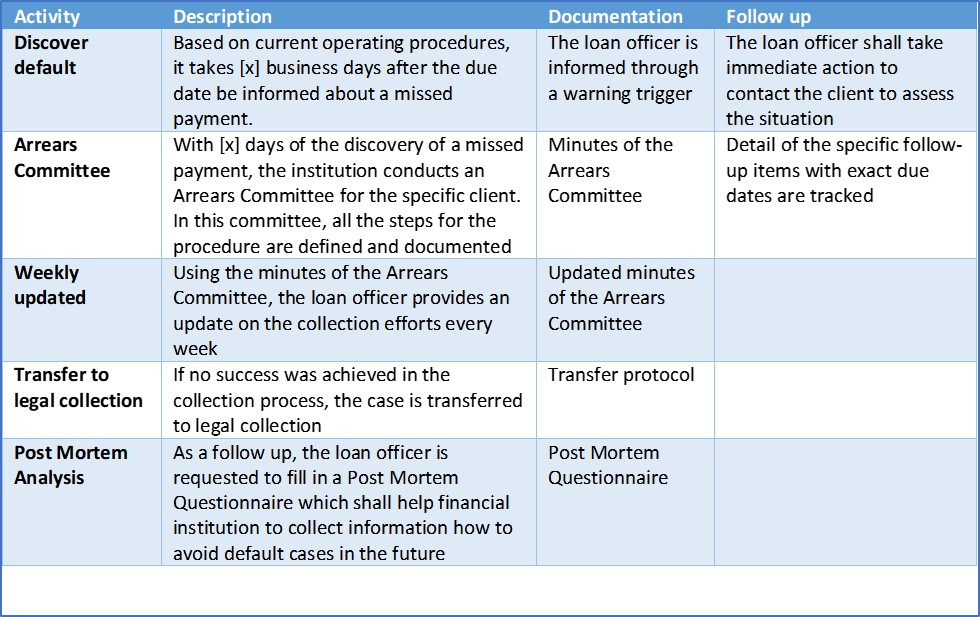

Loan Collection Process – Defaulted Loans Once a client is in default, the financial institution applies a strict procedure to collect the funds or to start additional measures quickly in case the collection seems difficult or impossible. The specific steps for the collection process depend on the financial institution. A sample process is described in the following table

Post Mortem Analysis – by closely analyzing defaulted loans and discovering the patterns behind defaults or the reasons, a financial institution can gain valuable information to improve the risk assessment of individual loans in the future. Reasons for defaults can be “avoidable mistakes” such as improper credit analysis and reliance on non-verified information, or “unavoidable reasons” such as sudden health issues for the borrower or natural disasters. [60] days after the default, the loan officer is required to fill the Post Mortem Questionnaire.

The Post Mortem Questionnaire are available to those loan officers who have loans with payments in arrears above 60 days. The loan officers have 5 business days to fill and return the questionnaires. The information is analyzed, aggregated and provided to the team as a training measure.

We believe in the high importance of a structured monitoring process, specifically in SME lending. While the initial analysis is important, the monitoring is even more relevant for the performance of the loan portfolio. Q-Lana takes this into consideration through the list of tools and instruments provided to the financial institution. Here even more the importance of knowledge-based credit risk management becomes obvious. The borrowing clients will appreciate the sophisticated approach to monitoring as this clearly positions the financial institution as partner to the business

About the author:

Christian Ruehmer is the Co-Founder and CEO of Q-Lana. Christian has over 25 years of experience in finance working for several large international banks in the areas or Risk Management, Credit Portfolio Management, and Investment Management. Christian has been an advisor in this sector, working with over 75 MFIs, banks, and international organizations, primarily in developing countries. He is the head of Risk and Compliance at Bamboo Capital Partners and sits on the board of several companies in the finance sector

About Q-Lana:

Q-Lana provides a digital platform to transform traditional lending into a knowledge-based, risk focused process. By digitizing the initial assessment, application and approval, monitoring and portfolio management process, as well as the collection, the financial institution generates significant knowledge about the performance and the credit quality of the target clients. This can be used to improve lending decisions, avoid losses and provide advanced support to the clients. Q-Lana replicates the existing lending process and allows for modifications to apply best practice. In addition, Q-Lana provides intelligent reporting and customized risk advisory. Q-Lana is based on a SaaS model that integrates well with existing core banking software and can be implemented within a 3-4 month timeframe.

Contact:

christian@q-lana.com