This is the fourth article in a series of blog posts in which we introduce the concepts of knowledge-based lending for SME business. In this article, we take a fresh look at the overall lending process in a financial institution focusing on SME loans. In each of the steps we show some ideas how to make the process more efficient and more substantial. We show how to improve the steps through the use of knowledge and contextual intelligence.

We have integrated all the ideas into the development of Q-Lana, the digitization platform for knowledge-based lending. Our clients apply those tools at their discretion, immediately or in future process improvements. We have developed Q-Lana as a comprehensive, fully customizable and intuitive, filled with smart tools and analytics to support financial institutions. For more information about Q-Lana, please read below and contact us

Simplicity and Speed vs Complexity and Completeness of Information

The knowledge about the SME business in the target markets is the greatest competitive advantage of SME focused financial institutions. The challenge is that this knowledge is mainly collected in the heads of the relationship managers and loan officers who deal with the clients for many years. Making this knowledge available within the institution can dramatically improve the quality of the risk assessment and provide superior service to clients.

The customer experience in financial institutions often lacks simplicity and speed. In this way, financial institutions give away their competitive advantages of maintaining a good relationship to other providers, specifically to those with ties to fintech. Offering streamlined application processes, transparent decisions, and simple terms and conditions for the products targeting SMEs is a way how a financial institution differentiates itself from its competitors.

Clients prefer simple and understandable products with transparent pricing. Most products can be classified into three basic forms of borrowing:

- Term loans in which a lump sum is received and repaid under certain terms and conditions

- Lines of credit which allow the borrowers to utilize and pay only for the amount that is needed

- Guarantee and insurance products in which no cash is exchanged initially, but the financial institution provides for specific contractually defined situations

Simplicity and speed in the decision process are often seen in the opposite of diligence and precision. The latter are key criteria for successful SME lending. When developing Q-Lana we did not compromise on quality and diligence of the assessment. Rather we used technology to simplify the collection and utilization of knowledge which will help the financial institution offering the precise products and services a specific client requires at a given point in time.

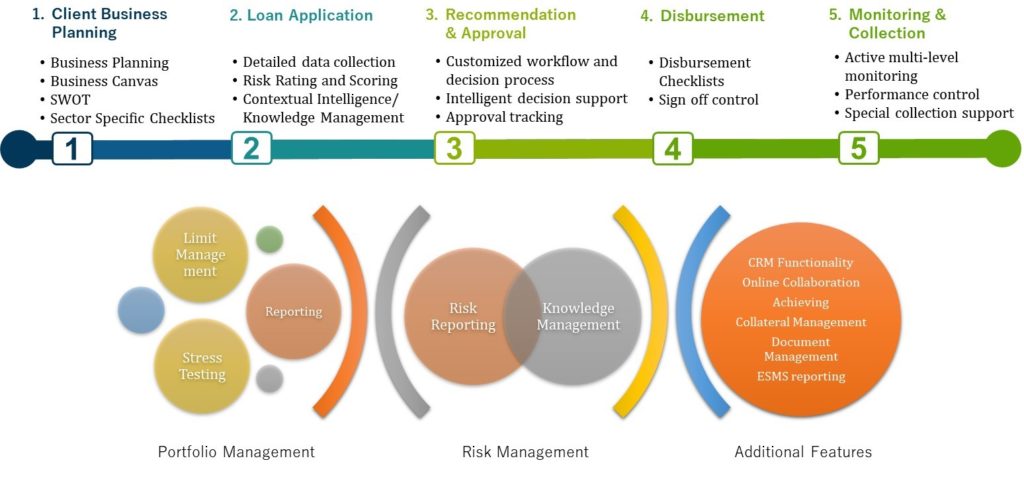

In the following, we pick out specific components of the lending process, where Q-Lana provides enhanced methods for the collection and assessment of client information. They are grouped in line with the process flow.

Company Analysis

To conduct the analysis of a company, Q-Lana provides several tools for the assessment of company, such as SWOT Analysis, Business Canvas, or Business Planning. The second part of this blog series provided the background to this. Q-Lana lifts these components even further as it provides the users the ability to search for assessments of comparable companies by sectors, regions or other criteria using contextual intelligence. Through such a peer assessment, the understanding for the specific situation of the client deepens and the loan officer can gain a better understanding of the companies in a certain sector or region.

The Q-Lana user has always access to the full resources analytics, training materials, instructions and background information. This information is provided through the research done by the financial institution as well as by Q-Lana’s Risk Advisory Services.

Risk Assessment

The analysis of the borrower’s financial information takes a key part in the assessment of credit risk in a loan request. The target clients of the financial institutions in developing countries might not have audited financial statements or no structured financial statements at all. In the development of Q-Lana, we have considered this potential challenge. Q-Lana supports analyst in the preparation of financial statements. Q-Lana uses a customizable Excel template to collect and analyze the financial statement in the required granularity. Calculations can be added, and ratios calculated on separate worksheets of the Excel file. The first worksheet of the template captures the summary. The loan officer can upload the template to Q-Lana, where the specific values are captured and stored. Once the upload is completed, the financial statement can be analyzed against comparable clients through the contextual intelligence.

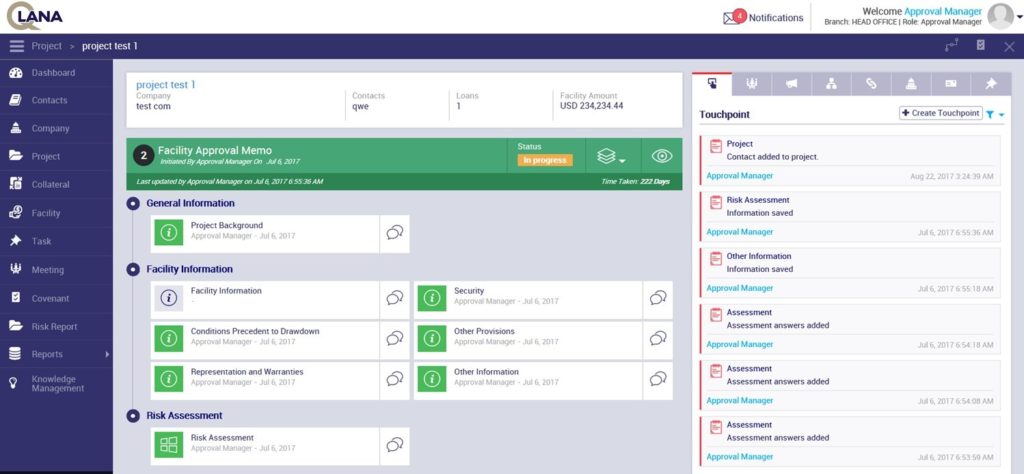

Q-Lana provides the ability to collaborate across teams in the assessment of a client and in the loan request. Questions can be raised across the network and comments provided on specific sections or the complete application.

A structured risk assessment is at the core of a loan request. Q-Lana provides a template for the risk assessment. The loan officer identifies the risks and categorizes them. The risks and mitigating factors are described, leading to a summarizing risk assessment. Over time, the financial institution builds a library of identified risks and can benchmark new transactions against the risk assessment of approved or declined loans.

As loan request moves through the approval process, the respective approval authorities can comment on the analysis, request further assessments, include specific approval conditions or forward the transaction after approval to the loan administration.

Approval

The fully flexible workflow functionality of Q-Lana allows the financial institution to replicate any type of approval procedures. Whether a department or a committee needs to approve the transaction or simply sign off on the request can be customized within the platform. The financial institution can define separate processes by product if the workflow differs.

As a loan request is forwarded for approval, the approval authority can compare the key components of the approval to other approved/decline transactions of the past. This will help with consistency of decisions and approval condition

Any decision is tracked within the Q-Lana platform, including the related minutes. In those minutes, conditions for the approval can be tracked.

Pre-Disbursement Checks

Once a request is approved, it is forwarded to the department preparing the disbursement. Here, the documentation is completed, collateral perfected and relevant copies are stored in Q-Lana’s document management functionality. Q-Lana maintains checklists, individualized for the institution, about the specific steps required before a loan can be disbursed. The completeness of the loan documentation can be monitored.

Q- Lana maintains a separate database for the management of collateral. Each collateral is tracked in the database and can be linked to to a specific transaction in the pre-disbursement process. The separation of the collateral management allows to track collateral in a more efficient way. Q-Lana allows to set reminders to update collateral documentation such as insurance certificates

Once a transaction is completed and disbursed, a dedicated monitoring and collection process follows, supported by Q-Lana. We have developed a monitoring process which keeps track of performing and non-performing loans. Through a combination of analysis of covenants, utilization, payment discipline and an early warning indicator checklist, loan exposures are tracked. Potential problems are identified and addressed before an actual payment default.

A detailed description of the monitoring process will be provided in the next blog article. Please contact us for comments and questions.

About the author:

Christian Ruehmer is the Co-Founder and CEO of Q-Lana. Christian has over 25 years of experience in finance working for several large international banks in the areas or Risk Management, Credit Portfolio Management, and Investment Management. Christian has been an advisor in this sector, working with over 75 MFIs, banks, and international organizations, primarily in developing countries. He is the head of Risk and Compliance at Bamboo Capital Partners and sits on the board of several companies in the finance sector

About Q-Lana:

Q-Lana provides a digital platform to transform traditional lending into a knowledge-based, risk focused process. By digitizing the initial assessment, application and approval, monitoring and portfolio management process, as well as the collection, the financial institution generates significant knowledge about the performance and the credit quality of the target clients. This can be used to improve lending decisions, avoid losses and provide advanced support to the clients. Q-Lana replicates the existing lending process and allows for modifications to apply best practice. In addition, Q-Lana provides intelligent reporting and customized risk advisory. Q-Lana is based on a SaaS model that integrates well with existing core banking software and can be implemented within a 3-4 month timeframe.

Contact:

christian@q-lana.com